This primer provides an in-depth look at different Private Equity (“PE”) strategies, including venture capital, growth equity, buyouts, turnaround strategies, PE fund of funds and secondary fund of funds.

Types of Strategies

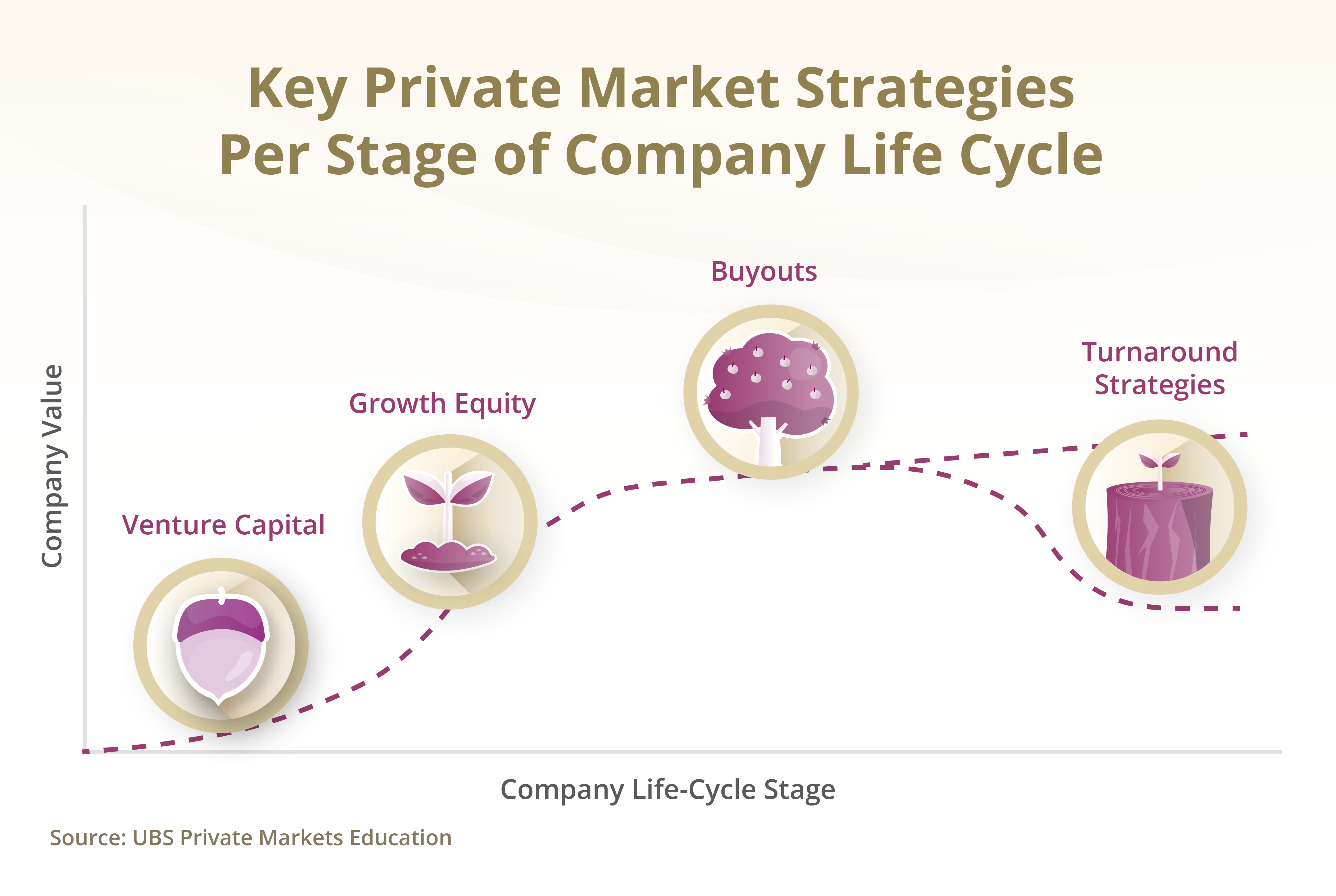

1. Venture Capital (“VC")

Venture capital focuses on investing in early-stage companies with high growth potential. VC firms provide capital, strategic guidance and networking opportunities to early-stage companies in exchange for equity. There are different stages of venture capital financing across angel, seed, early stage, late stage and expansion, which are reflective of a company’s maturity level. As a company grows, additional financing is provided in the form of ‘financing rounds’ to facilitate further development.

An iconic VC success story is Google, which received US$25 million joint funding from Sequoia Capital and Kleiner Perkins in its early financing rounds in 1999, when Yahoo was still the dominant player in the fragmented search engine market. Sequoia Capital and Kleiner Perkins’ investments eventually led to exponential returns for both firms upon Google’s IPO in 2004, becoming one of the greatest VC investments of all time.

Key Characteristics

- High Risk, High Reward: Early-stage companies present a significant risk due to their unproven models and competitive markets but offer the potential for outsized returns if they succeed

- Long-term Horizon: VC investments require a commitment to a longer holding period compared to buyouts, as startups often take time to develop their products, gain market share and become profitable

- Sector Specialisation: VC firms often concentrate on high-growth sectors such as technology, biotech, or green energy, which can experience rapid shifts and require deep industry knowledge

2. Growth Equity

Growth equity, which straddles between VC and buyouts, is a strategy where investors typically take a minority stake in relatively mature companies that are poised for expansion but are less established than typical buyout targets. Investors often adopt a passive role, preferring to keep the existing management in place to drive the company's growth. These firms are generally beyond the startup phase and are seeking capital to scale operations, enter new markets, or make significant acquisitions without altering the core structure or strategy of the business.

Airbnb, Spotify, and Uber are standout examples of companies that received crucial growth capital from TPG, a PE firm with a growth equity investment arm. At pivotal moments in their development, TPG’s investments enabled these firms to scale operations, expand into new markets, and refine their products and services. With this support, they evolved from promising startups into global leaders in their respective industries. TPG’s growth funds played a key role in driving the technological advancements and market expansions that powered the success of these iconic companies.

Key Characteristics

- Less Risk than VC: Companies are more established, reducing the risk compared to VC investments

- Balance of Debt and Equity: Growth equity deals often use a balanced mix of debt and equity, with lower levels of leverage used compared to buyout transactions

- Moderate Return Expectations: Returns are typically lower than VC but higher than buyouts

3. Buyouts

Buyouts, particularly leveraged buyouts (“LBOs”), involve the acquisition of a company, typically with a significant portion of the purchase price financed through debt. LBOs make up a significant portion of the global PE AUM. The acquired company's assets often serve as collateral for the loans. The PE manager executing a buyout aims to drive the company’s growth, profitability, and improve its market position, followed by a resale or public offering.

The acquisition of Hilton Hotels by Blackstone in 2007 is a classic LBO deal – financing was done with $20.5 billion (78.4%) debt and $5.6 billion (21.6%) equity. Blackstone utilised its expertise to restructure Hilton’s operations and strategically divest non-core assets. They also appointed a new CEO with experience in the hospitality industry to steer the business through the Great Financial Crisis. By the time Blackstone took Hilton public in 2013 and subsequently sold off its remaining shares, the firm had generated $14 billion in profit, almost quadrupling its original equity investment.

Key Characteristics

- Debt Leverage: LBOs typically involve high leverage, which can amplify returns but also increase financial risk if the company's cash flows fail to service the debt

- Target Mature Companies: Buyout targets are usually mature companies with established revenue streams and steady cash flows. These characteristics make it easier to service the debt incurred during the buyout process. The target companies often have significant assets that can be used as collateral for the debt and are seen as stable investments with potential for improvement

- Operational Improvements and Value Creation: Post-acquisition, the focus of a buyout strategy is often on improving the profitability and overall value of the acquired company

4. Turnaround Strategies

Turnaround strategies in PE involve investing in companies that are underperforming or struggling financially, with the goal of improving their operations and restoring profitability. PE firms with expertise in turnarounds will typically take an active role in restructuring the company's operations, management and strategy.

One of the turnaround stories involved Burger King, which was acquired by 3G Capital in 2010. Burger King was struggling with declining sales and an outdated image. 3G Capital restructured the company, revamped its menu and modernised its stores. The firm's efforts paid off when Burger King's profitability improved and it was able to go public again in 2012.

Key Characteristics

- Focus on Underperforming or Distressed Companies: Turnaround strategies involve investing in companies that are struggling financially or operationally

- Operational Overhaul and Restructuring: The strategy often includes a significant restructuring of the company’s operations, management, and strategy to restore profitability

- Potential for High Returns: While risky, successful turnaround investments can yield high returns due to the relatively lower entry valuations of distressed companies

Back to top

Types of Funds

1. Fund of Funds

PE fund of funds involve investing in a portfolio of PE funds rather than in individual companies. This approach allows investors to diversify their holdings across multiple PE strategies, geographic regions and industry sectors. Fund of funds managers select and combine PE funds to create a balanced investment portfolio of between 10 to 50 fund investments over several vintage years. Fund of funds are particularly suitable for allocators with smaller or less experienced investment teams who might not have the capability or resources to carry out the allocation process in-house. By entrusting a fund of funds manager to navigate the complexities of the PE landscape, these investors can benefit from a more hands-off investment approach while still gaining exposure to a variety of PE strategies and managers.

Key Characteristics

- Diversification: By investing in multiple funds across various PE strategies, geographic regions and industry sectors, funds of funds spread the risk across different managers and strategies. This diversification potentially lowers the overall portfolio risk

- Access to Top Managers: Fund of funds can provide access to top-performing PE firms and niche strategies that might otherwise be inaccessible to individual investors due to high minimum investment requirements

- Simplified Diligence Process: Investors in fund of funds only need to conduct a diligence process around the fund of funds manager they invest with. This manager then takes responsibility for sourcing potential investments, carrying out due diligence, and monitoring the other managers holding the investors' capital

2. Secondary Fund of Funds

Secondary fund of funds focuses on purchasing existing interests in PE funds from other investors who are seeking early liquidity by exiting before the end of the fund’s life.

Key Characteristics

- Accelerated Investment Pace: Unlike a primary fund of funds, which commits capital over time, secondary fund of funds provides immediate exposure to a portfolio of underlying PE fund investments

- Shorter Time to Liquidity: These funds typically have a shorter investment horizon as they invest in funds further along in their life cycle

- Discounted Prices: Secondary assets are often purchased at a discount to their net asset value

Wrapping Up

In summary, PE is not a one-size-fits-all asset class; it offers various paths for capital deployment and return generation. Building on this understanding of the diverse strategies within PE, it's important to delve deeper into the structural, economic, and relational aspects that underpin these investment approaches.

In our next discussion, we will explore PE fund structures, the economic dynamics at play, and the key players involved.

Back to top