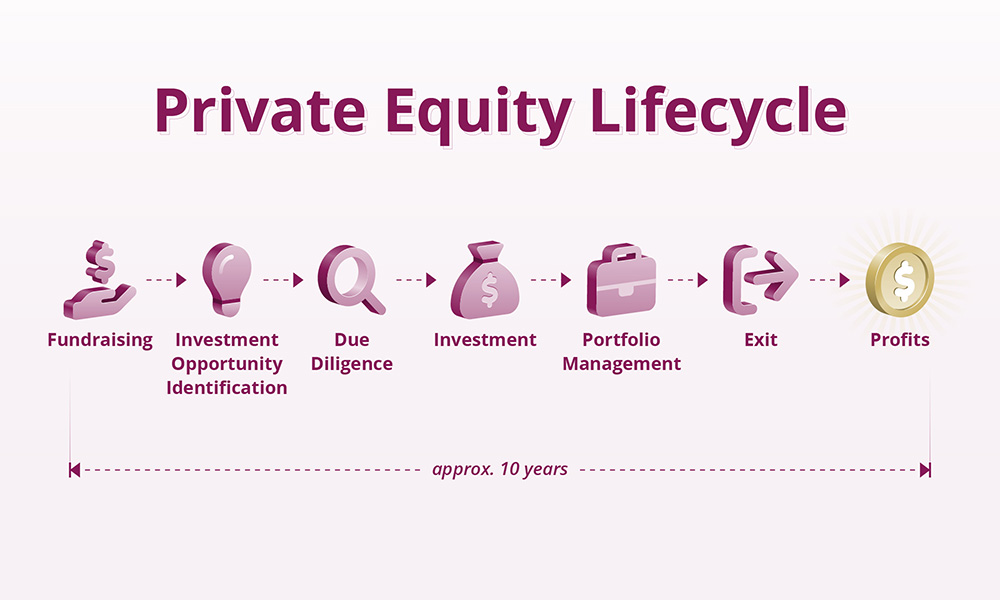

Private Equity (“PE”) firms invest in companies, aiming to generate returns for their investors by proactively making improvements and growing the companies before selling them at a higher value. This article, part of our Private Equity Primer Series, explores the PE investment lifecycle, highlighting the key stages and strategies for successful investments.

Back to top

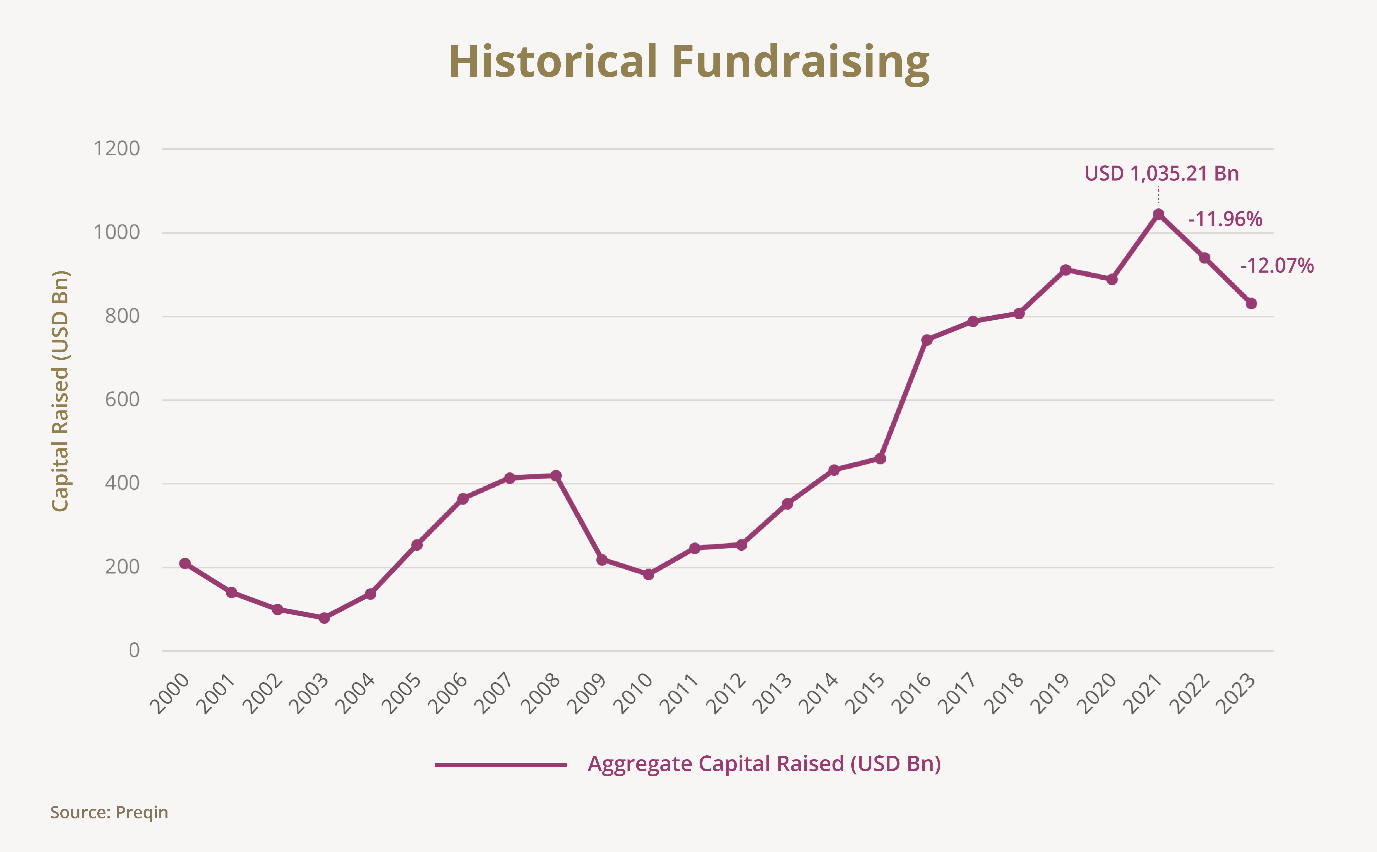

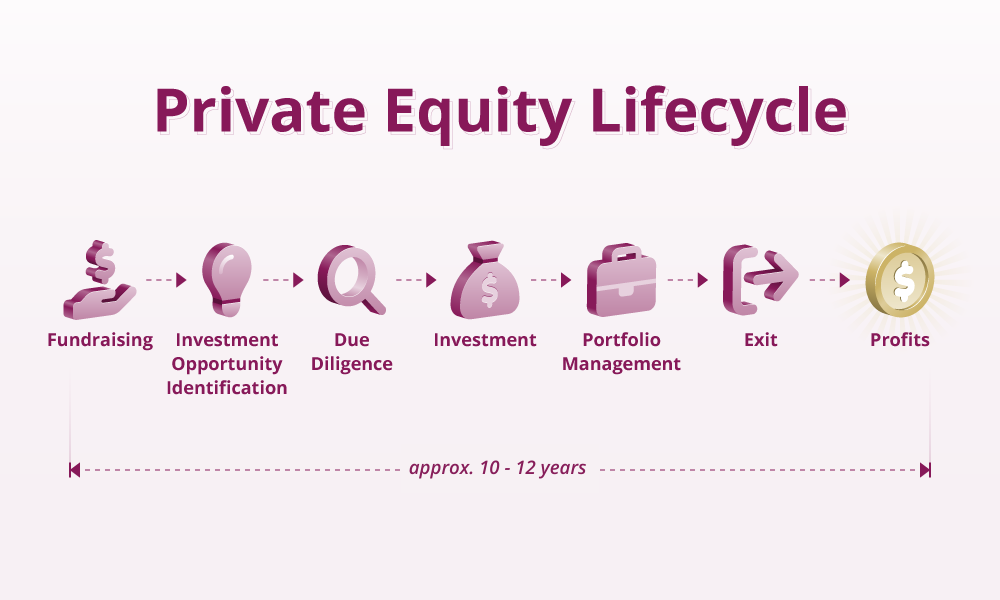

1. Forming the fund and fundraising

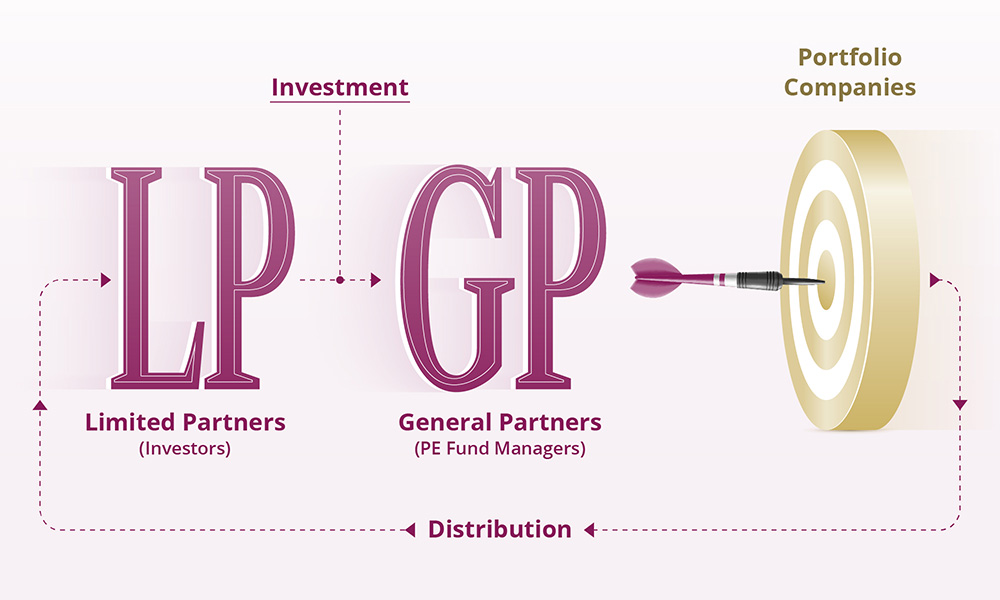

The initial phase of PE lifecycle involves the formation and fundraising of the fund. During the formation phase, the fund manager develops a strategic investment focus, establishes fund terms and prepares key offering materials like the Private Placement Memorandum (“PPM”) and Limited Partner Agreement (“LPA”). Following the formation, the fund enters the fundraising phase, where the manager approaches potential investors to secure capital commitments. The initial closing marks the start of the fund's investment activities, but fundraising often continues to meet the overall fundraising target.

Back to top

2. Identifying Potential Investment Opportunities

To generate returns for investors, fund managers will begin by scouting for investment opportunities that align with their strategy. They utilize a mix of methods including market research, professional networks, investment bankers, and direct outreach to potential targets. Advanced data analytics and AI tools are increasingly used to identify trends and promising sectors. Here are some of the traits that PE firms look for when identifying targets:

Historically Profitable with Cash Generation Potential

Fund managers favour companies with a history of profitability and cash flow generation, even if they're currently underperforming. A strong financial past suggests potential for future success.

Low Failure Risk with Strong Asset Base

Considering the leverage involved in PE deals, fund managers prefer companies with low failure risks and a substantial tangible asset base. These assets act as collateral for loans and ensure steady cash flow for debt repayment.

Opportunities for Productivity Enhancement

Fund managers often target companies with room for significant performance enhancements. Fund managers use their resources to drive productivity improvements through various levers such as operational enhancements, technology upgrades, and market expansion.

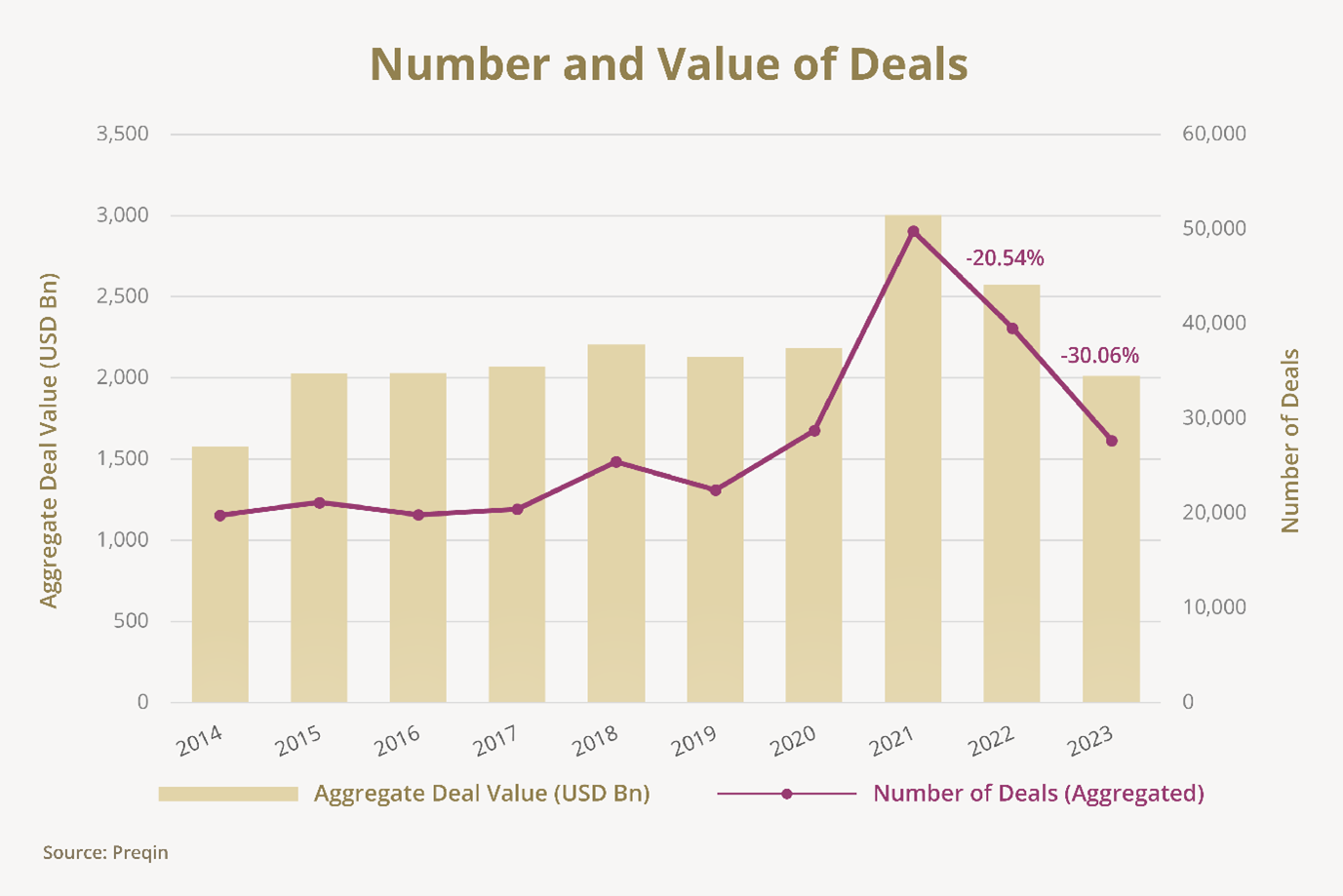

3. Performing Due Diligence and Acquisition

Once a fund manager identifies a potential target company, a comprehensive due diligence process is undertaken. This multifaceted approach involves examining various aspects of the target company to ensure a well-informed investment decision. Some of the factors considered are:

- Financial Performance, e.g. EBITDA and net profit margins, etc.

- Market Position and Competitive Landscape, e.g. market share, growth potential, etc.

- Legal Review, e.g. compliance, intellectual property concerns, etc.

- Operational Assessment, e.g. production efficiency, supply chain, management effectiveness, and cost structures, etc.

- ESG Evaluation, e.g. carbon footprint, adherence to reporting requirements, etc.

Based on the due diligence findings, the fund manager moves on to the acquisition process that involves finalising the acquisition structure, negotiating the final terms of the deal, including the purchase price, financing structure, securing necessary financing from banks or other financial institutions, and finally closing the deal.

Back to top

4. Adding Value and Managing Portfolio Companies

Post-acquisition, fund managers engage actively in the management of their portfolio companies. They might implement strategic changes, improve operational efficiencies, or streamline management practices. The goal is to increase profitability and growth prospects. Fund managers often leverage their network and expertise to provide strategic guidance, access to new markets, and additional capital for growth initiatives.

Case Study Snapshot:

One notable example of how a PE firm employ a mix of value creation strategies is the acquisition of a US-based discount retailer, Dollar General, by Kohlberg Kravis Roberts (KKR):

Dollar General Corporation is a discount retailer. The Company offers merchandise, including consumable items, seasonal items, home products and apparel. Its merchandise includes brands from manufacturers, as well as its own private brand selections with prices at discounts to brands1

1. Management Changes: KKR brought in a new CEO, Rick Dreiling2, who previously ran drugstore chain Duane Reade Inc. He and his new management team was instrumental in boosting sales and implementing operational improvements. The leadership change ensured effective execution of new strategies.

2. Operational and Product Optimisation: The new team and KKR streamlined Dollar General’s operations by improving supply chain management and reducing operational costs. Concurrently, they optimised their product mix, focusing on high-margin products like private-label goods, and streamlined their assortment by eliminating lower-performing items3.

3. Growth and Expansion: Dollar General's market expansion involved the addition of new stores and the remodelling of existing ones4, at a time when market conditions were favourable due to falling lease rates.

4. Debt Restructuring and Cost Management: Despite a substantial debt load, KKR effectively managed Dollar General’s financial leverage, improving its Debt-to-EBITA ratio5. Additionally, they significantly reduced shrinkage, which includes losses due to factors like shoplifting and mispricing, thereby saving considerable costs and contributing to the overall financial health of the company.

1 Reuters, 2024

2 Reuters, 2015, Dollar General says COO Vasos to replace Dreiling as CEO

3 The Wall Street Journal, 2009, Dollar General, Profiting on the Recession, Pays Off for KKR

4 The New York Times, 2007, KKR signs a record $6.9 billion buyout of Dollar General

5 The Wall Street Journal, 2009, Dollar General Is Paying Off for KKR Fund

Back to top

5. Exit Strategies

The ultimate aim of a PE investment is to realise a return on the capital invested. Common exit strategies include:

Initial Public Offering (IPO)

An exit strategy, particularly for large, high-growth firms, is taking the company public through an Initial Public Offering (IPO).

Strategic Sale

Another exit route is selling the company to a strategic buyer, usually a more substantial entity within the same industry.

Financial Sponsor Sale

In this scenario, the private equity (PE) firm might opt to sell its stake to another PE firm or a different financial buyer.

Recapitalisation

This strategy involves the company acquiring new debt to pay dividends to the PE firm, enabling the firm to realise part of its gains while still retaining ownership.

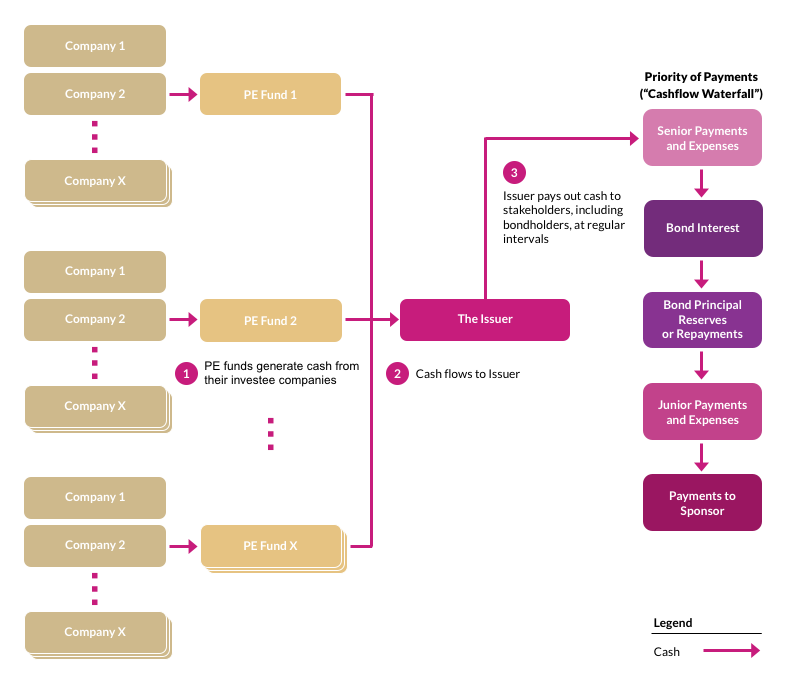

6. Distributing Profits to Investors

Successful exits transform long-term strategies into tangible financial rewards. When a PE fund exits its investments, the profits generated are distributed back to investors, typically through a waterfall distribution structure.

Wrapping Up

PE firms play a pivotal role in shaping the trajectories of their portfolio companies, driving not just financial but also operational and strategic transformations. It starts with identifying suitable investment opportunities, followed by thorough due diligence and strategic acquisitions. Post-acquisition, PE firms enhance company operations and financial health. The cycle concludes with well-planned exit strategies, allowing PE firms to realise returns and often leaving businesses stronger and more competitive, positively impacting the broader economy.